A ripple transforming into a giant wave!

ESG stands for Environmental, Social, and Governance. The global ESG market now accounts for over 30% of professionally managed assets in Europe, the United States, Canada, Asia, Japan, Australasia, and Africa (Source: Eurosif). The growth of the ESG market outpaces growth in the broader investment market.

Responsible investing has been around since the early 1970s but their popularity has increased considerably only over the last 10 years as investors become more conscious about the impact of their investment on the environment and humans. This is especially true for Millenials and women.

Millennials more responsible investors

Described as the generation born between 1980 and 2000, this generation is much more conscious about sustainability than the previous Baby Boomer generation. This is a structural shift in mindset that we believe is further strengthening with Gen X and Gen Y as collectively humans are becoming more conscious of the downside risk to the environment and social inequities incorporates and nations as well as the dubious methods adopted by some corporations in gaming the system.

That some of the biggest corporations (Tesla, Facebook) today have poor governance standards further adds to this ripple becoming a huge tide. One study indicates that millennials comprise 23% of all millionaires. Morgan Stanley surveyed 1,000 active investors in 2015 and 2017 and found that millennials were not only more interested in responsible investing (86% vs. 75% of the total population in 2017) but that their interest was growing. Between 2015 and 2017, the percentage of millennials who were “strongly interested” in sustainable investing jumped a massive 10 percentage points.

Women will control three-fourths of wealth in the US in 10 years

Women control nearly 30% or $39.6 trillion of the world’s wealth and 51% and $14 trillion of personal wealth in the United States. By 2020, that amount is expected to rise to $22 trillion. Over the next two generations, women are anticipated to inherit 70% of transferrable wealth and are expected to control about three-fourths of the wealth in the US alone. Women have a more emotional approach to investing than men, which is a great thing because they are not considering alpha generation as the sole factor behind investing but the ‘greater good along with reasonable returns’ as a bigger motive.

Enhances performance

What initially looked like a fad is slowly but surely transforming into a very important factor in selecting quality securities. Some argue that the CAPM model used in pricing assets is not optimal and it can be improved by adding dimensions such as sustainability. This has led to the growing adoption of Smart Beta in pricing securities.

Why ESG investing is here to stay

Great tool for making a portfolio less risky

Stocks with high ESG scores are considered to be less risky than peers. Companies with strong ESG characteristics typically have above-average risk control and compliance standards across the company and within their supply chain management (MSCI).

Due to better risk control standards, high ESG-rated companies suffer less frequently from severe incidents such as fraud, embezzlement, corruption, or litigation cases (cf. Hong and Kacperczyk [2009]) that can seriously impact the value of the company and therefore the company’s stock price. Hoepner et al. (2013) call this an ‘’insurance-like protection of firm value against negative events.‘’Less frequent risk incidents ultimately lead to the less stock-specific downside or tail risk in the company’s stock price.

Thus, adding high-rated ESG stocks lowers the risk profile of the portfolio and enhances its Sharpe ratio.

A portfolio with an ESG sprinkle outperforms

There are several studies conducted on the comparison of a high-scoring ESG portfolio with a traditional portfolio. Some findings are:

High ESG rating a good predictor of profitability. MSCI has concluded in a study that high ESG-rated companies (Q5) were more profitable and paid higher dividends, especially when compared to bottom quintile (Q1) companies.

Quality ESG companies have a lower cost of capital. Due to lower systematic risk as well as the inclination of investors and lenders to finance the company at a lower desired return, a quality ESG company has a lower cost of capital. It should be noted that this should transform to a higher valuation.

Survivorship bias, especially in Bonds

Companies that have quality ESG reporting are likely to be the ones that have invested more in this area and thus have information to share. Thus, a portfolio of companies that report decent ESG performance in itself will have a positive bias. Further, selecting companies above a minimum ESG score threshold will have a survivorship bias towards quality companies. This is especially true in the Fixed Income space – non-investment grade companies typically have very poor ESG reporting and thus selecting companies only on the basis of ESG reporting would leave one with mostly investment-grade companies.

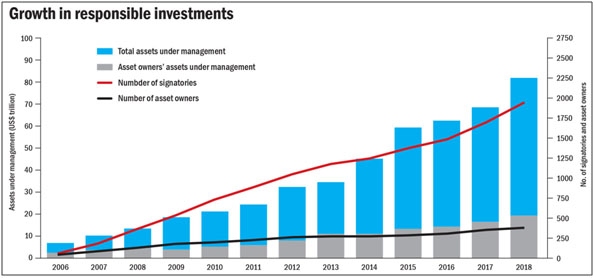

Huge swathes of investors joining the ranks

Since 1995, the US SIF Foundation first pegged the responsible investing universe at $639 billion. Over the next 23 years, this universe increased more than 18-folds to reach $12.0 trillion at a CAGR of 13.6%. Globally, the Socially Responsible Investing (SRI) AUM is estimated at $22.8 trillion. 40%of investors polled at a J.P. Morgan Macro Quant Conference in October 2017 are already investing in ESG strategies. As more investors develop awareness towards social, environmental, and governance practices of the companies they invest in, this universe is expected to continue to expand. This higher capital allocation towards quality ESG companies alone should lead to better price-performance and higher valuation.

Figure 1: Sustainable and responsible investing in the US (1995-2018)

How are asset managers factoring in ESG

Screening (in or out)

Screening involves selecting securities from a universe of investments that meet specific screening criteria determined by the investor. Exclusionary or negative screening excludes or underweights securities of certain countries or sectors. Inclusionary or positive screening, on the other hand, overweights securities that have a higher ESG score than peers. This used to be the predominant strategy but it led to a reduction in portfolio diversity as portfolios eliminated entire sectors and/or companies, which eventually led to underperformance.

ESG integrated investment

This strategy involves the systematic inclusion of all material factors that a company is exposed to. Two things need to be underscored –this method does not explicitly preclude “sin” sectors such as gambling or tobacco but analyzes each company on its ESG performance irrespective of its industry. Second, is the materiality of factors – not all ESG factors affect a company or an industry equally. For instance, energy management will be a significant environmental factor for a telecommunication company but not for airlines. On the other hand, labor safety would be a key concern for an airline operator but not for a telecommunications company.

An asset manager would include ESG as one of the key parameters in selecting securities. Since evidence points out that investable companies generally are also responsible companies, such an approach helps in building a superior “risk-adjusted return” portfolio.

SASB (Sustainable accounting standards board), from the Principles of Responsible Investing, mandates public companies in the US to report the materiality and how it impacts a company.

Figure 2: Example of SASB reporting

Source: Principles of Responsible Investing (www.pri.org)

ESG activist investing

Activist investors use their voting power and shareholding status to effect changes in the company’s future direction. Such investors can analyze a company’s ESG standing and then engage with the management to take steps for improving the company’s ESG performance.