Enhance the depth and breadth of your research efforts

Welcome to Equinox Research, your trusted partner in outsourced investment research for hedge funds. We offer a comprehensive range of research solutions tailored to meet your unique needs.

Limited bandwidth makes research ROI extremely critical

Research is the cornerstone of success for hedge funds. In this highly competitive and dynamic industry, the ability to identify opportunities, manage risks, and optimize returns depends on the depth and breadth of research. This is where Equinox Research steps in as your strategic research partner.

How We Can Help

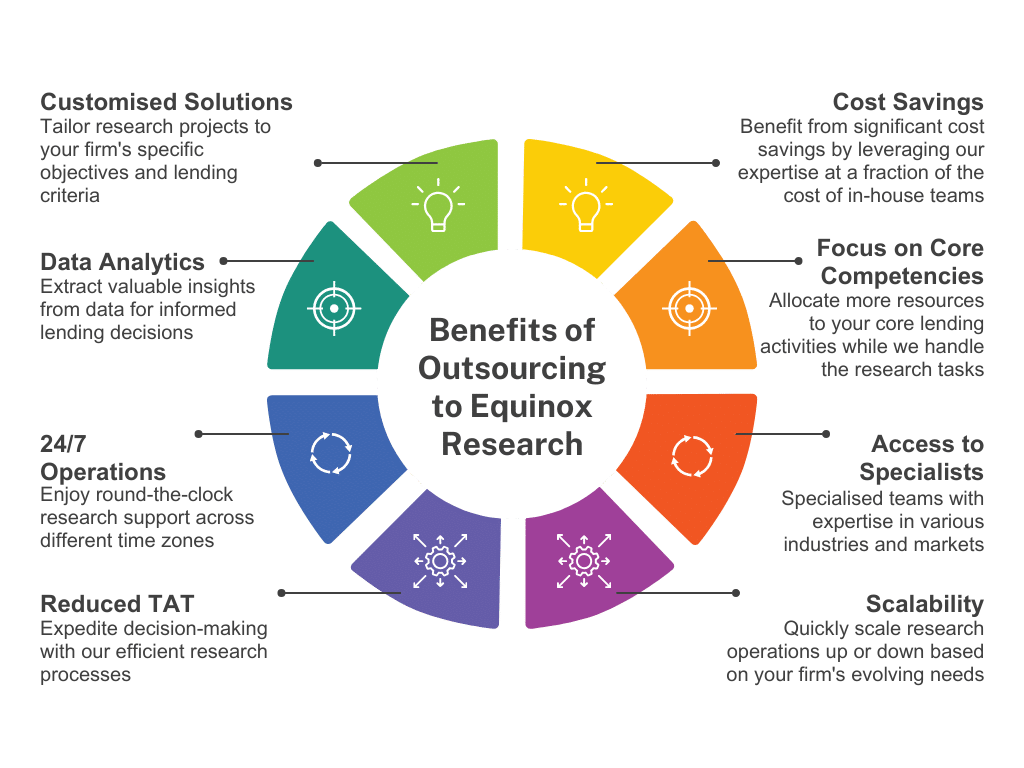

By outsourcing certain research functions to our specialized team, you can enhance the efficiency of your research efforts.